What is Deferred Revenue in SaaS?

Deferred revenue, sometimes called unearned revenue, is a core part of SaaS accounting because it reflects how subscription businesses deliver value over time. When a customer prepays for a product or service you’ll provide later, you can’t recognize that customer’s payment as revenue right away under accrual accounting and generally accepted accounting principles (GAAP). Until you deliver the service, the amount collected is an obligation to the customer and is recorded as deferred revenue on the balance sheet.

This article explains how deferred revenue works in SaaS, how it becomes recognized revenue, and how to keep your records accurate as billing schedules and contracts change.

Key takeaways

- Deferred revenue is money you collect before you’ve delivered the full subscription or service.

- Deferred revenue stays on the balance sheet as a liability until you earn it by delivering access or services over time.

- As you deliver each month (or milestone), part of deferred revenue becomes recognized revenue.

- Your invoicing schedule changes how deferred revenue rises and falls, even if the contract dates and total price stay the same.

- Clear recognition schedules and regular reviews help keep deferred revenue accurate when contracts renew, change, or cancel.

What is deferred revenue?

Deferred revenue is money you’ve already collected for a service you haven’t delivered yet, like an upfront subscription, gift card, retainer, or service contract. Even though you have the cash, it stays on your balance sheet as a current liability because you still owe the customer the service.

You recognize that revenue over time as you meet your performance obligation. For example, if a customer pays $12,000 on January 1 for a 12-month subscription, you’d recognize $1,000 by January 31 and keep the remaining $11,000 in deferred revenue until the rest of the service is delivered.

Deferred vs. recognized revenue

Deferred revenue is money you’ve collected upfront for a service you still need to provide, while recognized revenue reflects the portion you’ve actually earned by providing that service. As work is completed or time passes, amounts move from deferred revenue on your balance sheet to recognized revenue on your income statement, showing how revenue lines up with what you’ve provided.

Is deferred revenue a liability?

Deferred revenue is a liability under ASC 606/IFRS 15 because it reflects a promise your company has made to a customer, while the customer may record the payment as a prepaid expense. When you collect advance payments, you’re agreeing to deliver a product or service in the future. Until you do that, you still owe the customer something, even though the cash is already in your account.

As your team delivers the service, that obligation shrinks. Each month or milestone completed moves a portion of deferred revenue into recognized revenue, showing that your company has earned it by following through on what was promised.

The importance of deferred revenue for SaaS businesses

Deferred revenue matters in SaaS because customers often pay before you’ve provided the full service. Tracking it closely helps you stay clear on what you’ve earned, what you still owe, and what your revenue may look like for planning, financial health, and valuation as you continue providing value over time.

It also helps because it:

- Shows how much paid work you still need to deliver

- Helps with revenue projections

- Keeps reported revenue from looking inflated in the early months of a contract

- Makes it easier to match revenue to the period the customer is actually getting value

- Helps you plan headcount and costs based on what you’ve already sold

- Builds trust with investors, lenders, and auditors because your numbers line up with delivery

When you treat deferred revenue as a core SaaS metric, it becomes more than an accounting rule. It’s a simple way to understand how much business you’ve already secured and what your team needs to provide next.

Revenue Recognition Policy Template

Auditors require lots of documentation to ensure accuracy. Having a solid revenue recognition policy in place is the first step toward ensuring compliance.

How do you calculate deferred revenue?

Deferred revenue can be calculated with a simple formula:

Deferred revenue = Amount billed – Amount recognized as revenue

This tells you how much of what you’ve billed is still “unearned” because your company hasn’t delivered the related service yet. If the result is negative, it usually means you’ve recognized more revenue than you’ve billed, and that difference is typically recorded as unbilled accounts receivable, a current asset on the balance sheet, not accounts payable.

Common examples of deferred revenue

Here are two quick examples that show how deferred revenue changes based on when you invoice, even when the subscription value and service dates stay the same.

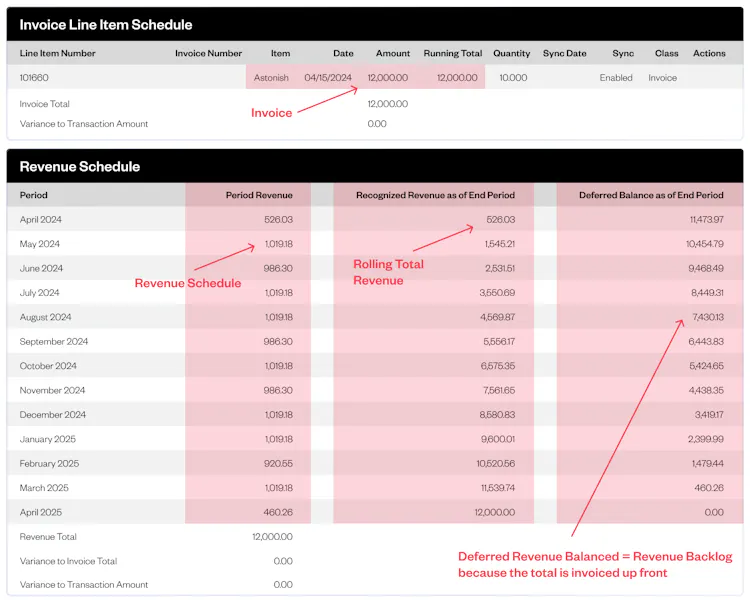

Example 1: annual subscription invoiced upfront

A one-year $12,000 subscription has:

- An order date of April 1, 2024

- A subscription start date and revenue start date of April 15, 2024

- A subscription end date and revenue end date of April 14, 2025

The subscription is invoiced on the subscription start date of April 15, 2024.

In this image, the invoicing schedule shows a single upfront invoice, while the revenue schedule shows revenue being recognized over time. Deferred revenue starts at the full invoiced amount and then decreases as revenue is recognized. April shows less recognized revenue because the subscription begins mid-month.

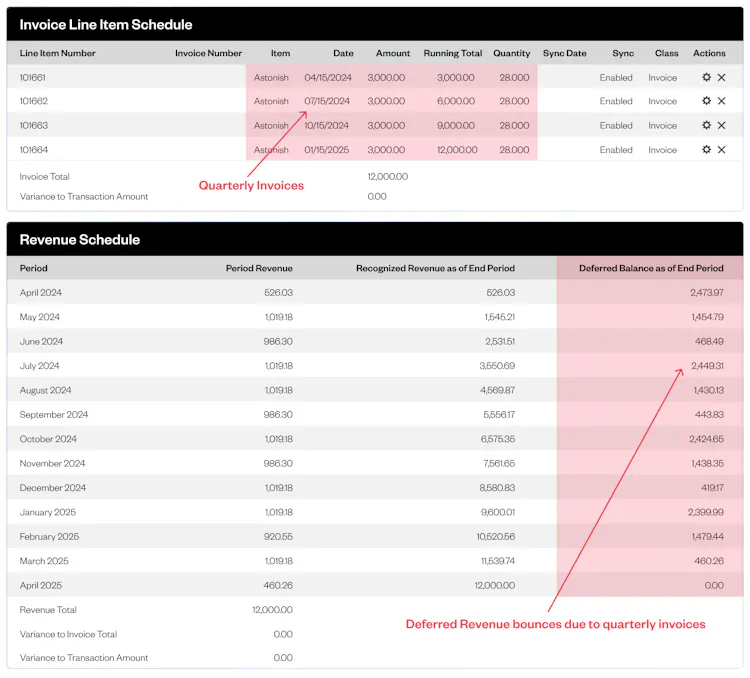

Example 2: annual subscription invoiced quarterly

In this example, the only change is invoicing. The subscription value and dates are identical, but the customer is billed quarterly over the term.

The revenue recognition schedule stays the same as Example 1, but the deferred revenue balance changes because billing happens in chunks. In the image, you can see deferred revenue increase when each quarterly invoice is sent, then decrease as revenue is recognized until the next invoice. That step-like pattern is the impact of quarterly invoicing.

Best practices for recording deferred revenue

Recording deferred revenue correctly keeps your financials accurate and makes it easier to understand what your company has earned versus what it still owes. These best practices help create consistency as subscriptions and contracts run over time.

- Align revenue to delivery: Recognize revenue based on when the service is actually provided, not when the invoice is sent, or cash payment is received.

- Maintain clear schedules: Use detailed recognition schedules that show how deferred revenue moves into earned revenue across the contract term.

- Review balances regularly: Check deferred revenue balances each accounting period to make sure they reflect active contracts and current delivery status.

- Coordinate across teams: Keep subscription billing, finance, and operations in sync, so contract changes, renewals, and cancellations are reflected correctly.

- Document your approach: Clearly record how your company handles deferred revenue so financial reporting stays consistent as systems and teams grow.

Following these practices helps ensure deferred revenue stays accurate and reliable. That accuracy supports better reporting and stronger confidence in your financial data.

Easily manage deferred revenue across all clients with Maxio

Deferred revenue sits at the center of subscription accounting. The amount you bill, the dates service is delivered, and the pace of revenue recognition all shape what shows up on your balance sheet each month. When you add real-world changes like upgrades, downgrades, credits, renewals, and mid-term edits, it gets harder to keep each journal entry clean and consistent.

Maxio gives you a reliable way to track deferred revenue without living in spreadsheets. The platform’s built-in revenue recognition software keeps billing and revenue connected, updates schedules when contracts change, and produces clear reports with a solid audit trail, so you can monitor deferred revenue alongside the other metrics your team relies on to track financial health without manual cleanup every month.

Get a demo to learn more about how you can simplify your revenue recognition and cash flow management at scale.

Revenue Recognition Policy Template

Auditors require lots of documentation to ensure accuracy. Having a solid revenue recognition policy in place is the first step toward ensuring compliance.