Growth vs. Profits in SaaS Company Valuations

Written in collaboration with Todd Gardner of SaaS Advisors.

Is profitability or growth more important to a SaaS company’s valuation in 2022? We looked at the correlation between growth and profits in public SaaS companies to find out.

Spoiler alert: it’s still growth

The short answer is growth is still 2.5 times more important than profitability in determining a SaaS company’s valuation.

Let’s dig into the data to see why.

In the current environment, the correlation between valuation multiples and growth rate is about .39. That’s the lowest correlation we have ever seen in the last 10 years, down from .57 at the peak of the market in November 2021.

If we factor in profitability by using the Rule of 40, the correlation to valuation multiples improves slightly to .42. That’s a little better than predicting the valuation multiple using just the growth rate, but not much.

Implicit in the Rule of 40, however, is that growth and profit are valued equally. A 1% higher growth rate impacts the metric as much as a 1% improvement in profit margin. That’s a pretty arbitrary approach.

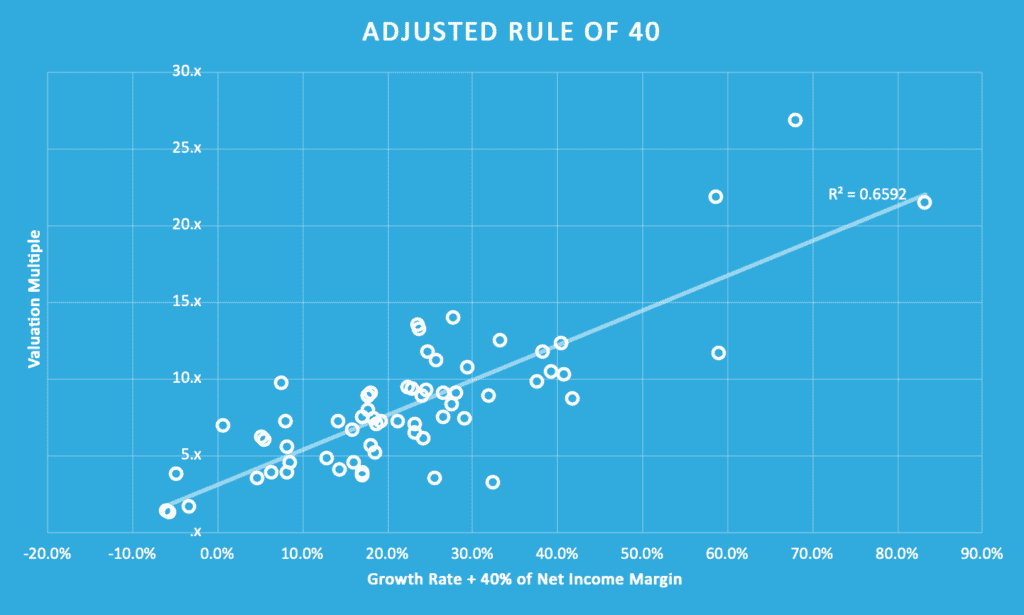

If you adjust the weighting, you’ll find that combining a SaaS company’s growth rate with 40% of its net income margin will yield a metric with the highest correlation to its valuation multiple. In fact, the r2 of this metric is currently .64.

Taking a step back, it’s important to remember that valuation multiples of revenue (or profits) are a short-hand form of estimating the future cash flow of a particular SaaS company. For most businesses, current profitability is the best proxy for future cash flow, so valuations are based on a multiple of profits. Multiples are higher for businesses whose profits are expected to grow and lower for those with lower future profit expectations. In both cases, the starting point is current earnings. This is commonly referred to as the price-to-earnings, or PE, multiple.

For most SaaS businesses, however, current profits aren’t the best indicator of future cash flows.

That’s because most SaaS businesses, even the public ones, haven’t reached maturity and are unprofitable or sub-optimally profitable. In this immature stage, investing in future growth generates more expected future cash flow (value) than generating earnings today. The important assumption here, and the only reason an unprofitable SaaS business has any value, is that SaaS businesses will eventually convert revenue into profits as they mature.

That assumption of profitability at maturity is well founded in the data. Ten of the twelve public SaaS companies founded before 2000 are solidly profitable, with an average net income margin of 17%, which is increasing annually. Conversely, only 11% of SaaS Companies founded after 2000 are profitable.

So what’s happened so far in 2022 to increase the relative value of profitability?

Two things:

1. Interest rates and inflation went up, making future profits less valuable than current profits. In valuation land, this means applying a higher interest rate to future earnings. So, the further into the future those earnings occur, the less they’re worth today.

The best proxy for when earnings will happen is the level of earnings today. For example, a company with a net income loss of 40% is less likely to generate profits as soon as a business with a net loss of 5%. Therefore, the more profitable a SaaS business is today, the sooner it’s expected to generate more of its earnings and the more it’s worth per dollar of revenue today (valuation multiple).

2. Risk appetite went down. This is a more straightforward lever. Unprofitable businesses run the risk of never becoming profitable, so their stocks are sold when risk appetite decreases. Unprofitable businesses may simply be immature, or they could have a business model flaw and run out of cash needed to reach maturity. Either way, they have a higher risk.

What does this mean for private SaaS businesses?

- The balance between growth and profits has shifted, but growth is still more important than profitability.

- If you can generate 1% or more of growth for each 1% loss in operating margin, you’re still creating real value. (Burn ratio)

- Percentages and ratios are great, but companies need to have cash for payroll. If capital is unavailable at any price, profits are your only alternative as a source of cash, even at the expense of growth.

The more mature the private SaaS business, the more relevant nuances in the public markets become. Early-stage SaaS companies should be aware of public market shifts and how they might impact funding sources. But the lag time between the early stage and the public markets is so long that reacting to each public cycle can be counterproductive to building the fundamentals of the business.

Regardless of your company’s growth stage, it’s important to understand the evolving relationship between growth rates and profitability on SaaS company valuations. So, to help you get a better handle on your path to growth, we’ve teamed up with Todd Gardner of SaaS Advisors to build this interactive Equity Calculator.

Fundamentally, this model compares selling your company today vs. raising capital, absorbing dilution, growing ARR, and selling in 24 months.

You can get access to the full Equity Calculator here.