Is AI’s influence on application software similar to the role open-source projects have played? And as the enterprise stack evolves, will it start to resemble the broader internet? I don’t think history repeats itself, but it can certainly provide context to help understand our current environment.

The Slowdown in SaaS

Growth in SaaS continues to decelerate. According to the most recent B2B Growth Report by Maxio, the median growth rate in 2025 was 18%. Is AI responsible for this slowdown? If so, how, and how much?

AI Software Replacement Theory 1.0

One argument for AI fundamentally disrupting software companies is that customers or startups can now replicate the code of established vendors at minimal cost, thereby undercutting those vendors in the market and taking market share.

This argument mirrors the longstanding impact of open-source projects and vendors, where free code bases have been available to users for years. In both AI-built and open-source scenarios, customers gain access to robust code bases with little to no financial investment.

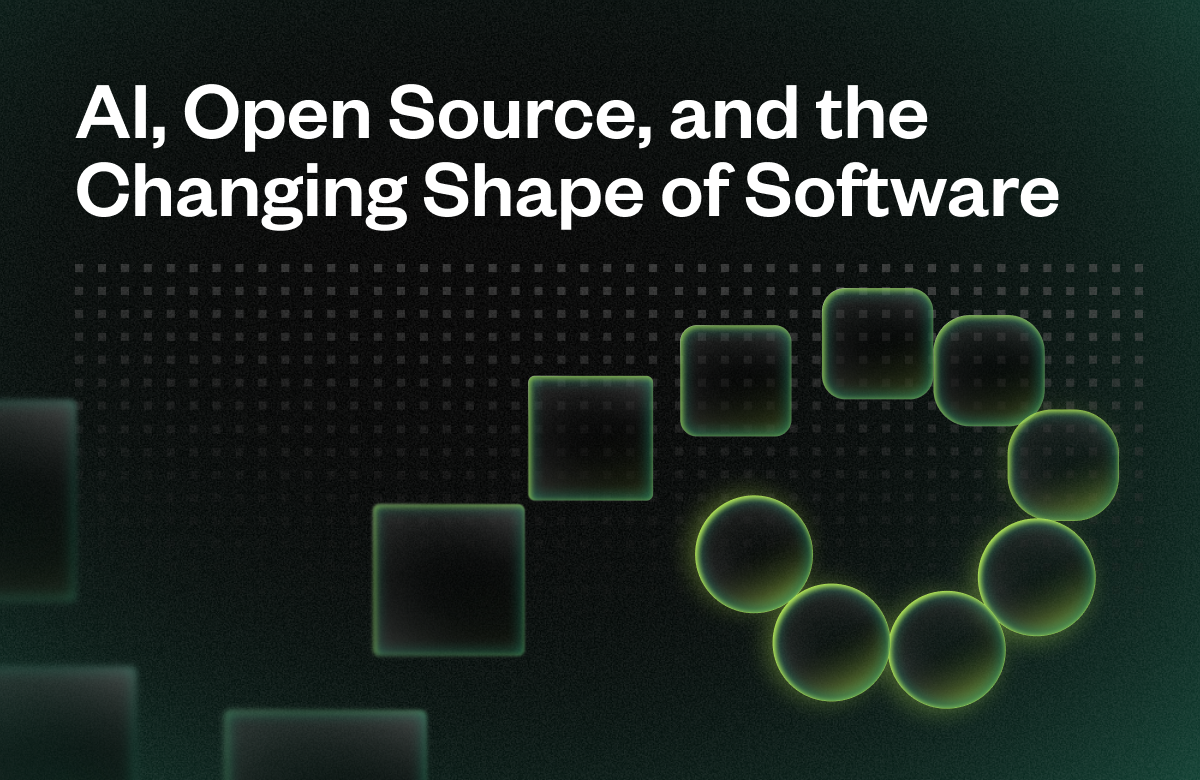

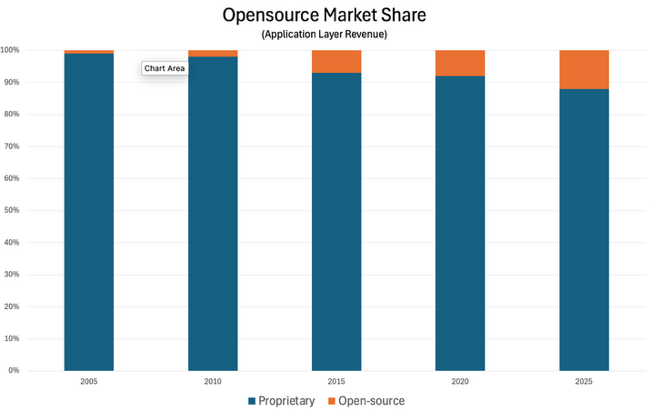

Open-source’s Limited Market Penetration

Yet, despite the availability of free code, open-source software has only captured a small fraction of the application software market over the past two decades, as measured by revenue. As shown in the chart, open-source represents about 12% of the market.

Why?

The answer lies in the additional services proprietary vendors provide. Beyond code, these companies offer implementation, training, support, hosting, stability, and accountability—services that free projects cannot match.

For an AI-native startup to compete successfully with established vendors, it would need to offer similar ancillary services. So, while an AI startup could replicate Salesforce’s code at a fraction of the original development cost, it must still build the rest of the company.

To be fair, open-source code is more ubiquitous than its revenue share in the application market would suggest. Open-source code is actually present in many application-layer products; it just no longer stands alone—it is now embedded in commercial products, just as AI code is.

Sunk Costs and Competitive Dynamics

Salesforce’s substantial investment in its code base represents a sunk cost; it’s no longer a protective moat, but neither is it a disadvantage, since the product is already built (to date). What matters now are future costs. If an AI startup and Salesforce both effectively leverage AI to reduce costs, they will face comparable ongoing operating expenses and compete on a fairly even playing field.

The big question is, can legacy vendors adopt AI as quickly as AI-native startups?

There are signs that it can. First, operating profits of public SaaS companies have recently soared. They are doing more with less, and while that is currently showing up as profit, it means their cost structure is fundamentally lower, and they are better positioned to compete with AI-native start-ups in the long run.

Second, some legacy SaaS companies have launched their own productive AI agents. Salesforce comes to mind. It has domain knowledge and customer access that most start-ups do not have.

Can legacy SaaS be nimble enough to beat the onslaught of well-funded AI native startups? It’s unlikely the answer will be binary.

Additional Threat #1: Direct Obsolescence

Some generic AI agents and tools can already do things better than software applications.

I’m not smart enough to name all the categories here, but tools like Financial Planning and Analysis (FP&A) strike me as vulnerable. I have heard finance professionals say that Excell plus Claude is better than any FP&A platform in the market today. I don’t know if that’s true, but it certainly represents an immediate threat. I’m sure other analytical software tools are vulnerable as well.

This is a threat companies can see coming, and churn in SaaS is slow at first, but I’m not sure there is a competitive response with a high likelihood of success.

Additional Threat #2: Software Irrelevance

The most significant threat to legacy application software is not AI-generated software but the potential irrelevance of all current software. AI is transforming the nature of work and data so profoundly that most current software may become irrelevant.

Let’s look at the last transformative technology wave, the internet, for clues.

Early internet “portals” (yes, that is what they were called) organized websites into categories like news, games, and weather. They were hard-coded directories for the content on the web. The early portals were soon disrupted by search technology and now by AI. The more powerful AI becomes, the less need there is for structure.

Like the early internet, enterprises today use distinct software for marketing, finance, and operations. With AI, however, it’s conceivable that the new enterprise technology “stack” will evolve into a unified data lake (similar to the broader internet). All of the enterprise’s data will be in one spot, and by all, I mean ALL. Customer data, marketing campaigns, usage, competition, phone calls, employee, billing, legal, product, and even the code base. The more data, the more robust.

Future software will be built around two things: building, tagging, and securing the data lake, and also the software agents that will mine the lake to perform corporate functions like sales, marketing, billing, and financial analysis. The enterprise will look somewhat like the internet, with agents browsing and editing the data.

While software will exist in this new construct, it will not resemble the solutions companies use today.

Disclaimer

Current blogs are full of predictions about the future of software in the AI age. And while I have laid out some arguments here, I really don’t know how it will all play out (nor does anyone else).

What I hope to do is provide context and historical frameworks to help operators and investors sort through the most likely threats so they can focus their resources there.